India has turned a new page in conducting financial transactions, courtesy of innovations such as the Unified Payments Interface (UPI). The National Payments Corporation of India (NPCI) rolled out UPI in 2016 with the aim of rendering financial transactions instant, frictionless, and low-cost. It allowed individuals to link their bank accounts to their smartphones, enabling easy transfers and payments without needing cash or cards. With UPI’s success, its adoption surged among urban consumers and large businesses, transforming the financial ecosystem.

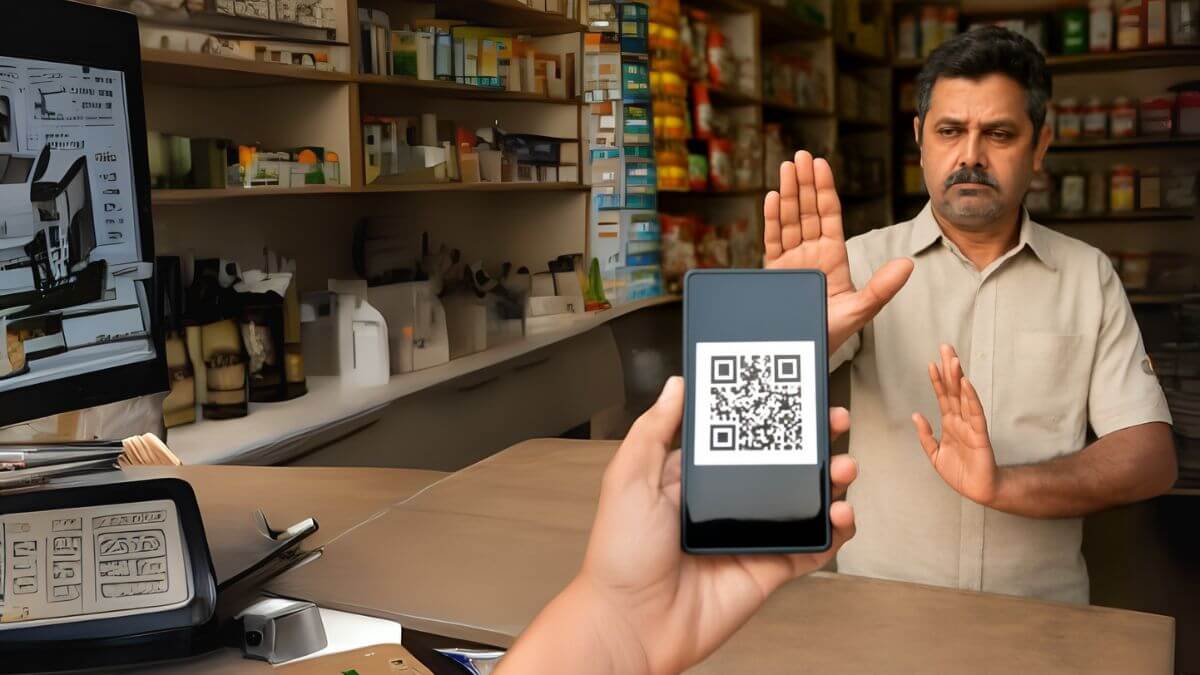

However, despite these advantages, many small traders, particularly those in rural and semi-urban regions, continue to resist adopting UPI payments.

Digital Illiteracy and Infrastructure Shortage

One of the biggest hindrances to UPI usage among small merchants is digital illiteracy. Most small traders, particularly rural and semi-urban ones, do not know anything about smartphones or digital payments. To them, acquiring the skills to associate bank accounts with mobile payment apps, handling UPI transactions, and operating digital platforms may appear challenging. Moreover, a significant proportion of India’s rural population does not have access to a stable and consistent internet connection, which further inhibits the adoption of UPI. Although penetration of the internet has increased over time, the quality and velocity of connections are still unbalanced, making it hard to rely on online payment systems for everyday transactions.

Resistance to Change and Cash Dependence

Cash is still the preferred choice of payment for most small vendors because of its immediacy and ease of use. Cash payments give them the feeling of control, and no intermediary system like a bank or a mobile app is required. Additionally, cash provides instant liquidity, which is important for traders who depend on immediate cash flow to fund their daily operations. UPI, while instantaneous regarding processing payments, does not offer the same immediacy regarding transferring cash into a trader’s bank account. In a few instances, funds do not show up in the account immediately and thus prove to be troublesome for traders to utilise the funds instantly. Such a delay in settlement is making the traders hesitate, as they feel it to be a hindrance rather than a convenience.

Perceived Costs and Bank Charges

As much as UPI has promised consumers and merchants free transactions, small traders find that there are hidden costs involved in embracing the system. While the fundamental UPI service can be costless, most small traders are apprehensive that their banks will charge maintenance fees for the accounts through which they make UPI payments, or that they will have to upgrade their current infrastructure, including acquiring a smartphone or subscribing to data connectivity. Such costs, although small compared to the potential benefits, seem to be inhibiting for traders already working on thin margins. They worry, even if the cost of digital infrastructure is low, that it will consume their margins.

GST Notices and Taxation Issues

One major worry for small traders who avoid UPI payments is the heightened emphasis on tax dues, especially under the GST regime. The Indian government has stepped up efforts to prevent tax evasion, and most traders have apprehensions that taking digital payments will bring them under greater scrutiny from tax officials. As UPI enables trackable, transparent payments, small traders fear their sales data will become readily available for tax officers to see. As a result, they could receive notices of non-compliance with GST or income tax laws, especially if they are lacking proper documentation or their revenues are less than the taxable levels. These tax-related issues have discouraged numerous traders from embracing digital payment methods, opting for cash payments instead, which are more difficult to trace and report.

Low-value, high-volume transactions are common among small traders, especially in retail, hospitality, and services. For them, the prospect of getting GST notices for not being able to fulfil tax payments may instil a high level of resistance against implementing UPI payments. The tax audit fear, fine, and legalities involved in GST registration and compliance scare many traders away from embracing digital payments. This problem is aggravated by an ignorance of how to account correctly for and report digital transactions within the GST framework, also deterring traders from utilising UPI.

Trust Concerns and Fraud Fears

Even with the strong security measures in place for UPI, small traders are still apprehensive about fraud. Phishing scams, illegal transactions, and identity theft are all areas of concern for novice traders who are not familiar with the security that UPI has in place. Small-scale traders can worry about being targeted by fraudsters who impersonate customers or payment service providers if they do not understand the mechanisms of digital payments. Unsolicited fund transfer fraud, improper merchant verification fraud, and other similar fraudulent activities involving UPI further complicate these issues. In the absence of good knowledge of digital security, merchants may be afraid to trust a system that appears to be confusing and replete with pitfalls. The lack of understanding regarding how UPI’s two-factor authentication process works, as well as the general fear of technology, makes the system seem too risky for many traders to adopt.

Unstable Cash Flow and Delayed Settlements

Many small traders face the problem of managing tight cash flows, where the timing of payments and the immediate availability of funds are crucial. While UPI facilitates instant payments, the funds might not reach the merchant account instantly. Settlement delays are reported by some traders, in which the funds do not appear in their bank accounts for several days or even hours. This is especially an issue for small traders, who need to access their earnings immediately in order to pay for daily expenses, including replenishing inventory or paying suppliers. Merchants who have been used to getting instant cash payouts feel that UPI, with its minor lags, disrupts the smooth operation of their business.

Consumer Behaviour and Cultural Factors

There are cultural reasons behind the resistance to UPI payments as well. Across much of India, especially rural India, cash is culturally established as the method of transaction. Customers are more used to cash as it is safer and more conventional. Digital payments, on the other hand, seem to deviate from conventional practices, and most customers might not believe in digital systems. Traders, then, will be reluctant to spend money on UPI systems if they are certain that their customers are not knowledgeable about or keen to use them. This is exacerbated by a lack of general awareness about UPI, especially in rural and small-town areas, where consumers continue to use cash and are not aware of the advantages of digital payments.

Fear of Increased Competition and Investment Required in Digital Infrastructure

For small merchants, there is also apprehension that the implementation of UPI payments might compel them to overhaul their overall business model, and that might cost money and be effort-intensive. They are not keen on spending money on smartphones, high-end point-of-sale machines, or other infrastructure needed to accept digital payments. Small traders are apprehensive that they would be pushed into greater competition by big businesses or that they would fail to compete with already more technology-oriented traders. Consequently, the cost of switching to a digital payment system seems too great in relation to the gains, and traders are more likely to remain with the tried and tested traditional ways.

Consequences of Avoiding UPI for Small Traders

The decline in the implementation of UPI payments has a wide-ranging impact on small traders. By not accepting digital payments, traders restrict their customer base, especially since urban consumers are increasingly embracing cashless transactions. Small traders who fail to take UPI might lose considerable business prospects, as more individuals are moving towards digital payment modes. Also, by not using UPI and other electronic payment platforms, traders remain outside the institutional financial system, whose restrictions on access to credit, loans, and other financial instruments may bind them.

Also, being outside electronic payments, traders remain in the cash economy, in which fraud, robbery, and inefficiency become more common.

Conclusion

While UPI has been welcomed as a groundbreaking move toward India’s transition into a cashless economy, the avoidance of digital payments by small merchants is still a major problem. The adoption obstacles—running from inadequate digital literacy and infrastructure to tax concerns, scams, and disruption of cash flows—keep inhibiting the proliferation of UPI among small businesses. To address these challenges, focused awareness campaigns, enhanced internet connectivity, and more definitive guidance on tax compliance and security features will be required. With appropriate support, small traders can be enabled to adopt UPI, facilitating new growth opportunities and a more inclusive and efficient economy.